Phone 0 Down Payment: A Practical Guide to Smartphone Financing

Learn how phone 0 down payment deals work, the hidden costs, and how to compare offers. Your Phone Advisor breaks down total cost, APR, and term length to help you decide smart financing.

Phone 0 down payment means you get a phone without paying upfront, but you’ll pay the device off in installments with interest over the term. While it lowers immediate cash outlay, it can raise the total cost depending on APR and contract length. Promos vary by carrier, so compare APR, term length, and early-termination rules before deciding.

What the term 'phone 0 down payment' really means

In everyday shopping, a phone 0 down payment means you can walk out of the store with a new device without putting any money on the table upfront. Instead, the cost is spread over a term through monthly payments or financing. This approach is popular with carriers and large retailers because it lowers the initial barrier to entry, but it does not make the phone free. The total price you pay is the sum of monthly payments, financing charges (APR if applicable), and service plan costs embedded in the agreement. According to Your Phone Advisor, the main benefit is improved cash flow in the short term, which is useful when you’re budgeting tightly or need to upgrade quickly. The catch is that long-term costs can rise if APR isn’t truly promotional or if you’re locked into a lengthy contract you don’t intend to honor. When evaluating a phone 0 down payment option, ask: What is the APR and how long is the term? Are there penalties for early termination? Is there a buyout option at the end, and what would the total cost be across the life of the agreement?

How carriers structure 0-down deals

0-down offers are typically presented as a device financing or leasing option rather than a traditional purchase. Terms commonly range from 24 to 30 months, with monthly device payments that replace an upfront price. Promotions may include 0% APR for a limited period, after which the APR can jump to a higher rate. It’s crucial to read the fine print because some deals disguise interest in the form of maintenance fees, mandatory insurance, or stacked plan costs. The language used by carriers can vary—some label it as a “device payment plan,” others as a “finance agreement.” Regardless of naming, the meaningful figures are the monthly payment, the contract length, and the final buyout or ownership rights. When you compare phone 0 down payment offers, map out the annual cost per device and total payments over the term. This helps you see beyond the sticker price and understand true cost of ownership.

Costs beyond the upfront zero

Choosing a phone 0 down payment option shifts the cost from your wallet today to a series of monthly charges, which means you should think about the total cost of ownership. APRs, even during promotional periods, can affect the bottom line; if the promo ends, the rate may increase significantly. Don’t forget ancillary costs such as device protection, extended warranties, activation fees, and required service plans. If you miss a payment or break a term, penalties can compound quickly. Insurance often becomes mandatory in 0-down deals to protect the device, adding to the monthly burden. Your total spend over two to three years can be substantially higher than a straightforward upfront purchase, depending on the specifics of the contract and whether you plan to upgrade or keep the device long term.

0-down vs leasing vs financing vs subsidized plans

When you see a phone 0 down payment offer, you’re often choosing among several financing structures. A true purchase via upfront payment means owning the device outright from the start and paying only service charges thereafter. Leasing typically offers lower monthly payments but requires returning the device or paying a sizable buyout at the end. Subsidized plans can pair a reduced upfront cost with restrictions on device upgrades and usage. In all cases, calculate the total cost over the term, not just the monthly bill. If your goal is flexibility and the option to upgrade frequently, a 0-down lease or financing option could be attractive, but you should compare with a straightforward upfront purchase to see where you land in total expenditure over the same period. This comparison is central to smart decision-making about the phone 0 down payment option.

How to evaluate 0-down offers

To evaluate a phone 0 down payment deal, start by calculating the all-in cost. Gather the monthly device payment, the contract length, and the APR (or note that it is promotional). Then add potential service plan fees, insurance, and any activation charges. Create a simple model: multiply the monthly device payment by the term, add any non-monthly fees, and compare that total to an upfront purchase scenario plus the same service plan costs. Consider whether you truly need the upgrade cycle you’re committing to—if you don’t plan to upgrade within the term, the total cost may be higher than anticipated. Finally, read the fine print for early termination penalties and buyout terms at the end of the contract. This disciplined approach is essential when weighing the phone 0 down payment option against other paths to the device.

Real-world scenarios and decision guide

Imagine you’re weighing a phone 0 down payment offer because your cash flow this month is tight. If you expect to upgrade within 18 months, the 0-down path might be compelling because you avoid a large upfront cost and minimize immediate outlay. However, if you plan to keep the same device well beyond the term, it can be more economical to pay upfront and avoid ongoing financing charges. In another case, a consumer prioritizing predictability prefers a traditional plan with a fixed monthly payment and a clear ownership path at the end. Across these scenarios, compare not only the monthly payments but also the total cost over the period you intend to own or upgrade. Accurate comparison for the phone 0 down payment decision hinges on honest budgeting and a clear upgrade plan.

Common pitfalls and red flags

Beware of phone 0 down payment offers that include opaque terms, hidden fees, or automatic add-ons in your monthly bill. Always verify the ownership rights at the end of the term and whether a buyout is required to keep the device. Watch for bundled insurance or protection plans that inflate the monthly payment without delivering proportionate value. Some promotions impose usage restrictions or limit upgrade options, tying you to a particular network or device type. Before signing, request a transparent itemized quote showing upfront costs (if any), monthly device payments, any APR, service plan charges, and the final buyout or ownership terms. Clear, apples-to-apples comparisons are the best defense against overpaying with a phone 0 down payment deal.

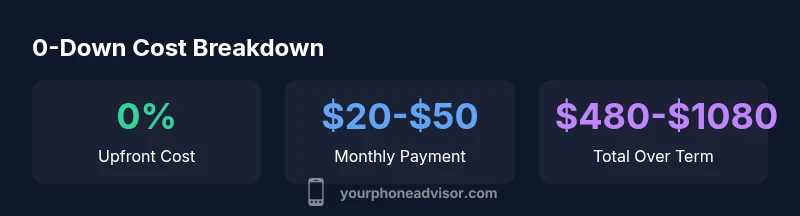

Comparison of common phone purchase options

| Option | Upfront Cost | Monthly Device Payment | Total Over Term | Notes |

|---|---|---|---|---|

| 0 down financing | 0 | $20-$45 | $480-$1080 | Shifts cost to monthly payments; watch APR |

| Traditional upfront purchase | $600-$1,000 | 0 | $600-$1,000 | Owns device outright; no financing costs |

| Lease | 0 | $25-$60 | $600-$1440 | Possible mileage/usage restrictions; may have buyout |

Got Questions?

What is meant by a 0 down payment for phones?

A 0 down payment means you don’t pay upfront for the device. Instead, you pay monthly payments over a set term, often with interest or financing charges. Ownership rights and final buyout options vary by contract, so read the fine print. Your Phone Advisor recommends confirming total cost and ownership terms before agreeing.

A 0 down payment means no upfront cost, but you’ll repay the device monthly, possibly with interest. Check the total cost and ownership terms before signing.

Are 0-down offers always cheaper in the long run?

Not necessarily. While the upfront price is lower, the total cost can be higher if the APR is high or if you’re locked into a long contract. Always compare the total payments across the same ownership horizon.

Often not—zero upfront doesn’t guarantee lower total cost. Compare total payments over the term.

Will I own the phone after the term ends on a 0-down plan?

Ownership terms vary. Some 0-down plans require a final buyout or transition to service plans to keep the device, while others may give you ownership automatically after the term. Read the contract to confirm.

Ownership depends on the contract—some require a buyout, others transfer ownership automatically.

What happens if I miss a payment on a 0-down deal?

Missing a payment can trigger late fees, increased APR, or termination of the agreement. Some programs also impact device eligibility for upgrades. Stay current or contact the lender to review options.

Missing payments can trigger penalties or termination—stay current or contact support to discuss options.

Is 0-down financing available for all phone models?

Not all models are offered with 0-down financing. Availability depends on the carrier, retailer, and current promotions. Alternatives include leasing or traditional financing for specific models.

Not all models are offered with 0-down financing; check promotions for each model.

How do I compare 0-down deals across carriers?

Create a side-by-side across monthly payments, contract length, APR, and final buyout terms. Include any mandatory insurance or service plan costs, then calculate the total cost for a 24- or 30-month horizon.

Compare monthly payments, APR, term length, and buyout to see which deal truly saves money.

“"0-down deals can be a cash-flow tool, but they shift cost and lock you into long contracts. Always calculate total cost and compare terms before committing."”

What to Remember

- Calculate total cost, not upfront price

- Watch for promotional APR periods

- Match term length to upgrade plans

- Consider total ownership costs, including insurance

- Avoid terms with heavy early termination penalties